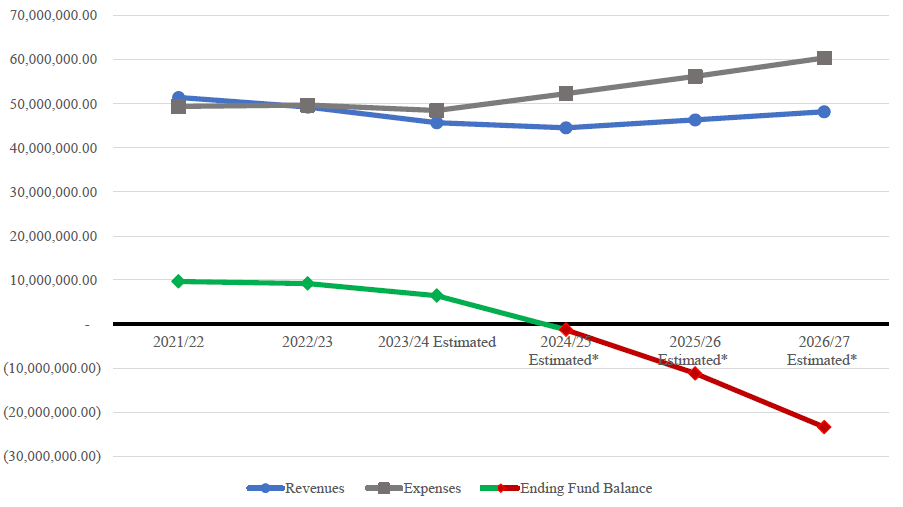

Without additional revenue, the compounding nature of the County’s projected financial shortfalls will lead to drastic changes in the services the County can afford to provide residents. These changes may include a reduction in the level of public safety available and a reduction in any non-constitutionally mandated services the County currently provides (e.g., Sheriff Road Patrol). Reductions can include a combination of eliminating vacant positions, employee layoffs, reductions in hours of operation, and/or the sale of assets. Apart from securing additional revenue, the only path forward is a significant reduction in County staff and services, which will impact all residents of Eaton County.